Stablecoins as Private Cash: Part I

Stablecoins are a form of private money - that is, money issued by private entities. Modern examples of private monies include commercial bank deposits and money market fund (MMF) shares, but there have been other forms of private money issued throughout history. One of the most colorful time periods is the issuance of various paper currencies by private banks during the Free Banking Era in the United States.

Public money, on the other hand, is a liability of, or issued by, a government institution. Examples of public monies include US Treasury bills (T-bills), bank reserves, and physical currency. Public money differs from private money in several ways, but one of the most important is that public money from a highly-rated sovereign issuer is generally thought to be free from nominal default risk.

Public money has an important backstop that private money does not.

This context is important, especially in light of Terra’s recent collapse.

The Free Banking Era in the United States

Shinplasters, shingles, stump tails, and red dogs are some of the names given to paper money issued by US state banks during what is known as the “Free Banking Era,” the brief period in US history from 1837-1863 when US banks were fairly unregulated and allowed to issue their own currencies. As the derogatory-sounding nicknames for their currencies imply, on balance, allowing such freedom in banking did not work terribly well – many free banks closed and many more of their banknotes were unable to hold their value.1

The conventional explanation for why this happened is fraud. Lack of government intervention is said to have encouraged dishonest bankers to form “wildcat banks.” These were banks formed only to defraud the public by issuing notes they would never redeem in specie (gold or silver). While there are a variety of apocryphal tales about how banks were supposed to have carried out this fraud, one of the most popular is that these banks discouraged attempts at redemption by setting up offices in areas populated by wildcats – that is in dangerous places, far away from the community where they circulated their banknotes. These wildcat bankers then profited by quickly closing the banks after the banknotes had all been circulated, disappearing with the banks’ assets.2

Even aside from the banks which operated as outright frauds, there were many more banks that simply went bankrupt as a result of capital losses suffered due to substantial drops in the price of the state bonds that free banks were required to hold as collateral. Falling collateral prices would precipitate runs on these banks – noteholders would attempt to go to the bank as soon as possible to redeem notes for specie at par. Oftentimes, these notes would close with market values below par, reflecting the relative riskiness of the issuing bank.

Furthermore, in addition to the credit risk associated with the ability to redeem the banknotes at par as a result of potential solvency issues, there was also liquidity risk associated with the ability to use banknotes far from their origin. A bank’s notes might well be used in transactions at locations far from the bank, but rather than trading at par value, the notes would trade at discounts from par at such locations.

For example, discount rates for Indiana banks’ notes were quoted in New York City. If the discount rate was 1.5 percent for a bank’s notes, a person in New York City with $100 in Indiana notes could exchange them for $98.50 of specie.

Usually, the discount reflected the transportation cost and interest forgone due to the time required to return the notes. Notes issued by banks that were likely to fail traded at discounts greater than usual even before closing. These excess discounts reflected the probability of failure, the payment that noteholders expected to receive, and the interest forgone while waiting for the payment.3

Modern-Day Private Cash

The example of the Free Banking Era above provides a somewhat extreme manifestation of how private money works. To simplify a little, private monies are financial liabilities of private entities, bearing a promise to be redeemable at par to other more accepted forms of currency upon request. They are often interest-bearing.

This definition itself brings up several questions:

What kind of entities can, or would want to, issue private money?

How does society agree that such entities should be allowed to issue private money?

Why would we want to redeem it at par to another form of currency? Does this imply that the private money in question is somehow inferior to that other form?

What sort of risks do the interest rates on these forms of private cash reflect?

In the United States today, two forms of private cash dominate the economy: bank deposits and money market fund (MMF) shares.

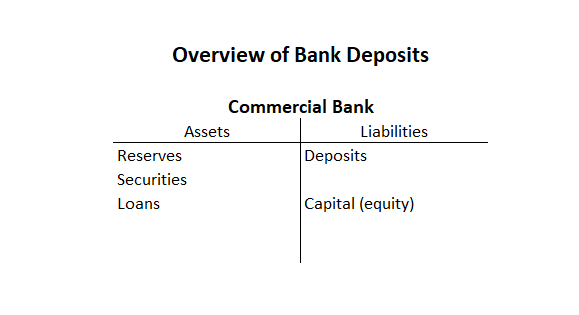

As shown in the stylized balance sheet diagram above, banks issue deposits to fund a variety of assets, including loans. The use of bank deposits to fund loans involves credit, maturity, and liquidity transformation.

Credit transformation refers to the enhancement of the credit quality of debt issued by the intermediary through the use of priority of claims. For example, the credit quality of deposits is better than the credit quality of the underlying loan portfolio, owing to the presence of more junior claims.

Maturity transformation refers to the use of short-term deposits to fund long-term loans, which creates liquidity for the saver but exposes the intermediary to rollover and duration-mismatch risks. Demand deposits are withdrawable on demand but loans must be funded for their entire duration (which may last months or years).

Liquidity transformation refers to the use of liquid instruments to fund illiquid assets. For example, the use of liquid demand deposits to fund a pool of illiquid whole loans exposes the bank to sudden withdrawals of funding in the event of a crisis of confidence.

These fundamental risks in the structure and composition of bank balance sheets expose depository institutions to the risk of bank runs, thus necessitating the implementation of deposit insurance. Moreover, there are a variety of other guardrails that place limits on other aspects of bank balance sheet construction, including capital requirements on both risk-weighted assets (RWA) and non-risk weighted leverage ratios, as well as liquidity requirements governing the composition of banks’ assets. These regulations limit the riskiness of the assets banks can hold relative to a base of equity capital, and their total leverage (total assets/equity), as well as require banks to hold a large percentage of their investable assets in so-called “high-quality liquid assets” (HQLA), which primarily include reserves and USTs.

One of the most important characteristics of money is the ability for it to trade at par on demand. In the context of bank deposits, this means that they are always redeemable for physical currency or deposits at another bank.

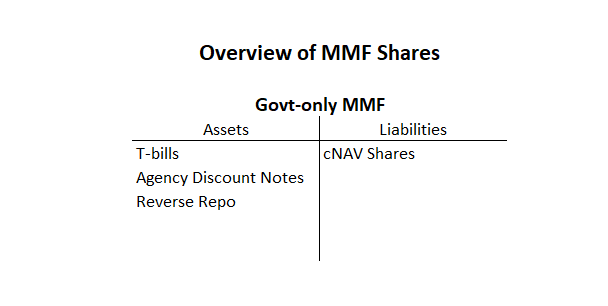

The function of Money Market Fund (MMF) shares, as the diagram above shows, is similar to, but not exactly the same as, bank deposits.

MMFs engage primarily in maturity transformation – not credit or liquidity transformation. MMFs invest in short-term securities or loans, such as T-bills, agency discount notes (discos), and reverse repos. These securities and loans typically have a maturity from a few weeks up to a year, while their constant net-asset value (cNAV) shares are redeemable on demand, like bank deposits.

Since their holdings are essentially credit risk-free and highly liquid, they do not have to worry about the same credit and/or liquidity risks that traditional depository institutions face.

However, MMFs have had significant problems in the past, including in the 2007-2008 Global Financial Crisis (GFC). The perception of MMFs as a potential source of systemic risk requiring heightened regulation became prevalent following the announcement in September 2008 that the Reserve Primary Fund would “break the buck” and the subsequent run on MMFs.

The risks exposed by the GFC led to the implementation of 2a7 reforms in October 2016. There are several aspects to these reforms, but most importantly, they require MMFs to hold at least 10% of their assets in daily liquid assets and 30% of their assets in weekly liquid assets. These requirements are designed to support funds’ ability to meet redemptions from cash, or securities convertible to cash, even in market conditions in which money market funds cannot rely on a secondary or dealer market to provide liquidity.

The other important difference between MMFs and banks is that MMFs use equity (cNAV shares) to fund their assets, in contrast to banks, which overwhelmingly use various forms of debt/liabilities. In other words, cNAV shares are not liabilities of MMFs, but deposits are liabilities of banks.

As stated earlier, one of the most important characteristics of money is the requirement for it to trade at par on demand. In the context of MMF shares, this means that they are always redeemable for bank deposits.

In a nutshell, banks and MMFs are commercial entities whose balance sheets are designed to take specific types of credit and/or liquidity risks. Their business models involve harvesting the spread (or risk premium) between the asset side and the liability side of their balance sheets. Any risky commercial activity requires a system of controls and guardrails. Over time, the US government has developed regulatory frameworks for these categories of entities, overseen by a (somewhat confusing) array of regulatory bodies such as the Federal Reserve, Treasury, FDIC, OCC, and SEC.

Modern private monies are a product of public-private partnerships. Both sectors are required to create the secure network effects needed.

Par and the Hierarchy of Money

In September 2007, television viewers and newspaper readers around the world witnessed an old-fashioned bank run – that is, depositors waiting in line outside the branch offices of a UK bank called Northern Rock to withdraw their money. The last UK bank run prior to Northern Rock was in 1866. The problem was that, in contrast to FDIC insurance in the United States, UK bank deposits were fully insured only up to £2,000, and then only 90% of the deposits up to an upper limit of £35,000.

When depositors were faced with the possibility that Northern Rock might fail due to the freezing up of short-term funding markets, the incentive for retail depositors to withdraw their funds was overwhelming (even though by the summer of 2007, only 23% of Northern Rock’s liabilities were in the form of retail deposits).

This example demonstrates that when the perceived credit quality of an issuing bank comes into question, depositors rush to withdraw their deposits. If other banks were also perceived to be in danger of failing, most depositors would prefer physical currency (which is a liability of the central bank) over deposits at another bank (which are simply liabilities of a different commercial bank, but still subject to some credit risk).

Bank runs, and the frenetic chaos they invoke, reveal a subtle truth. At times, some banks’ deposits are preferable to or safer than others, even though they are supposed to trade at par.

Bank runs clearly illustrate the point that private monies carry credit risk. When confidence in the issuing entity disappears, private money holders seek the safety of a “higher” form of money (i.e. one issued by a more creditworthy entity). In the Northern Rock example above, that more creditworthy entity was the Bank of England, whose banknotes were in demand by the depositors that fateful morning.

Now, consider a hypothetical scenario for what happened that morning at Northern Rock branches throughout the UK. Suppose Northern Rock had run out of physical currency, but offered to present Her Majesty’s Treasury-issued 1-week T-bills (in old-school bearer form) instead. Presented with that alternative, or no withdrawals at all, it is highly likely that everyone in line would accept this choice, because those T-bills can be redeemed for Bank of England-issued cash within a week.

However, if you took a £100 note to the Bank of England and asked to redeem it for “money,” all you would get is a blank look and the same £100 note in return. In a developed economy where the viability of the central bank is not in question, central bank-issued cash is the highest form of money. It is so because the law says so. That is why it is called “fiat” – everyone else in that jurisdiction, including the taxman, is legally obliged to accept it as a means of payment.

Stablecoins as Private Money

Private entities like Tether and Circle are the largest issuers of stablecoins today. Their liabilities – the stablecoins – are the latest iteration of private monies described above. Their respective pegs to the US Dollar are simply another manifestation of the promise for holders to redeem at par.

While individual mechanisms differ, these stablecoin-USD pegs are generally held by a combination of arbitrage incentives and beliefs in their respective reserve backings. Fiat-backed stablecoins, such as Circle’s USDC and Tether’s USDT, rely on their holdings of actual USD assets against their respective on-chain stablecoin liabilities. Algorithmic stablecoins – like Terra’s UST, which very recently collapsed spectacularly – relied on little to no hard asset backing. Algorithmic stablecoins, instead, rely only on market participants’ incentives to arbitrage any deviations from the stated peg, which in turn depend on their beliefs that the peg would ultimately hold.

Other stablecoins fall in between these examples. FRAX, for example, uses a fractional reserve system to balance run risks against scalability. Maker mints its stablecoin DAI against “vaults” of cryptocurrency collateral, relying instead on over-collateralisation to ensure peg stability.

All private monies come with risk. In particular, stablecoins suffer from the same kind of run risks as other forms of private money (commercial bank deposits, MMF shares, etc.), as well as their own unique set of risks, which include the risks of smart contract hacks/exploits.

In the next issue of Unpegged, we will dive more deeply into the specific kinds of risks that different types of stablecoins suffer from. We will discuss the backing of centralized stablecoins like USDT and USDC, conduct a brief post-mortem on Terra’s collapse, offer an explanation of where interest rates on stablecoins come from, and delve into more detail on blockchain-specific stablecoin risks.

However, there is more nuance to this claim than is commonly acknowledged/accepted. A large portion of the blame for these fraudulent wildcat banks can arguably be placed on inconsistent or poorly designed regulation as opposed to a lack of regulation. For example, the provisions of free banking required that all free banknotes must be backed by state bonds that the wildcat banks would lose if they did not redeem their notes.

There were states that allowed banks to issue notes equal to the par value, instead of the market value, of the bonds deposited with the state auditor. When the par value of the state bonds was significantly greater than the market value (i.e. the bonds were trading at distressed levels), the notes of free banks located in these states might not have been fully backed.

Arthur J. Rolnick, Warren E. Weber, “Free Banking, Wildcat Banking, and Shinplasters” Federal Reserve Bank of Minneapolis Quarterly Review, Vol. 6, No.3, Fall 1982.

Gerald P. Dwyer Jr., “Wildcat Banking, Banking Panics, and Free Banking in the United States,” Federal Reserve Bank of Atlanta Economic Review, December 1996.

This is really great. Clearly written and provides useful historical context without going overboard into detail.

This, is being so enlightening to me. Thank you. And your writing style is simple, impeccable.